OBR forecasts long but shallow recession

Updated projections from the Office for Budget Responsibility (OBR) suggest the UK is facing a long but relatively shallow recession which will see households hit by a record drop in living standards.

Chancellor Jeremy Hunt unveiled the independent fiscal watchdog’s latest forecasts during his Autumn Statement delivered to the House of Commons on 17 November. Mr Hunt said the country was facing “unprecedented global headwinds” before announcing the OBR’s new figures which show the UK entered recession during the third quarter of this year.

The updated predictions suggest the UK economy will expand by 4.2% across the whole of 2022, but then shrink by 1.4% next year before returning to growth in 2024. This implies that the downturn will be relatively shallow, if long by historic standards.

Although the recession is forecast to be comparatively shallow for the economy as a whole, the household sector is expected to be hit particularly hard due to a combination of factors including soaring energy and food prices, rising interest rates and higher taxes. As a result, the OBR figures suggest households are facing the largest fall in living standards on record.

Prior to the Chancellor’s Statement, the latest gross domestic product figures from the Office for National Statistics (ONS) had revealed that the UK economy shrank in the three months to September. ONS said the economy contracted by 0.2% across the third quarter of the year driven by a decline in manufacturing which was evident ‘across most industries.’

Survey data also suggests the economy continued to shrink during the first two months of the fourth quarter. The headline reading of S&P Global’s Purchasing Managers’ Index, for instance, sank to a 21-month low of 48.2 in October and November’s preliminary reading rose only marginally to 48.3. Any value under 50 represents economic contraction.

Bank Rate hiked sharply

Last month, the Bank of England (BoE) sanctioned a further increase in its benchmark interest rate and said more rises were likely but not to levels that had been priced in by financial markets.

At a meeting which concluded on 2 November, the BoE’s nine-member Monetary Policy Committee (MPC) voted to raise Bank Rate by 0.75 percentage points to 3.0%. This was the eighth consecutive increase since December and the largest rate hike since 1989. In addition, minutes to the meeting stated that a majority of MPC members believe ‘further increases in Bank Rate may be required for a sustainable return of inflation to target.’

However, the minutes also pointed out that the peak in rates is expected to be lower than markets had been anticipating. Indeed, in an unusually blunt message delivered when announcing the rate decision, Bank Governor Andrew Bailey said, “We can’t make promises about future interest rates but based on where we stand today, we think Bank Rate will have to go up by less than currently priced in financial markets.”

The next interest rate announcement is due on 15 December and economists expect MPC members to sanction another increase in rates – in a recent Reuters poll, more than three-quarters of all economists surveyed predicted rates will rise by 0.5 percentage points, with all of the other respondents predicting a 0.75 percentage point increase.

Comments made during the last few weeks by a number of MPC members have also reaffirmed the need for further rises in order to return inflation to the central bank’s 2% target. Some members, however, including BoE Deputy Governor Dave Ramsden, have begun to mention the possibility of rate cuts at some point in the future, should economic conditions diverge from current expectations and “persistence in inflation stops being a concern.”

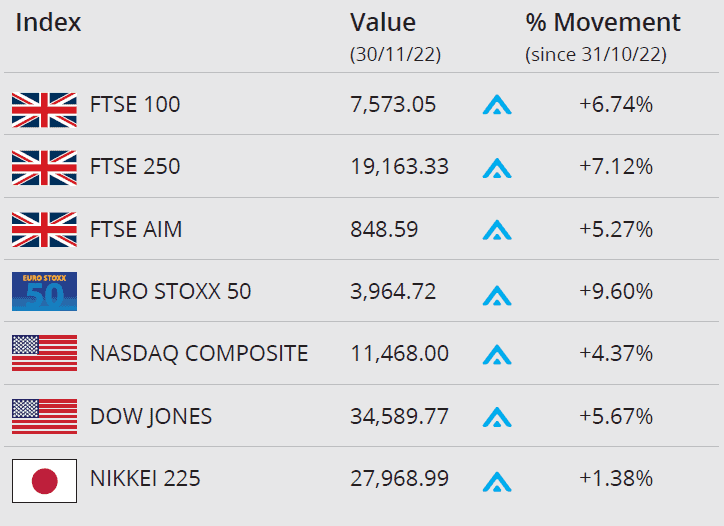

Markets

Global indices largely closed November in positive territory. In the UK the FTSE 100 advanced, ending the month at its highest closing level for five months, supported by commodity and energy stocks. The blue-chip index closed the month up 6.74% to 7,573.05, while the mid-cap FTSE 250 gained 7.12% and the FTSE AIM ended the month up 5.27%.

On Wall Street, markets closed sharply higher following Federal Reserve Chair Jerome Powell’s speech on 30 November, indicating the central bank might scale back the pace of its interest rate hikes as soon as December. The Dow closed the month up 5.67% on 34,589.77, while the Nasdaq closed November on 11,468.00, up 4.37%.

At the end of November, European Central Bank President Christine Lagarde said that a more hawkish line on rising inflation was needed on the continent, suggesting that more rate hikes are likely in the coming months. The Euro Stoxx 50 closed the month up 9.60%. In Japan, the Nikkei 225 closed November up 1.38%.

On the foreign exchanges, the euro closed at €1.15 against sterling. The US dollar closed the month at $1.19 against sterling and at $1.03 against the euro.

Brent Crude closed the month trading at around $86 a barrel, a loss of 5.32%. Signs of an oversupplied market earlier on in the month pushed prices lower but it recovered in recent days as discussions on a Russian price cap continue and government data showed US stockpiles plunging, while traders accelerated buying amid optimism that China will soon loosen restrictions. Gold is currently trading at around $1,753 a troy ounce, a gain of 6.99% on the month.

Record pay growth still lags inflation

While the latest earnings statistics revealed regular pay is now rising at a record level, the data also showed wage growth is still failing to keep up with the rapidly rising cost of living.

ONS figures released last month showed average weekly earnings excluding bonuses rose at an annual rate of 5.7% in the three months to September. This was the strongest recorded growth in regular pay witnessed outside of the pandemic when the data was distorted by workers returning from furlough.

However, although the rate of pay growth is currently high by historic standards, wage increases are still being outpaced by spiralling inflation – in real terms, regular pay actually fell by 2.7% over the year to September. This represents a slightly smaller decline than the record fall recorded three months ago but is still among the largest falls since comparable records began in 2001.

The latest official inflation statistics also revealed a further jump in price growth during October, with soaring energy bills and food prices pushing the annual figure to a 41-year high. The headline rate of Consumer Price Inflation rose to 11.1% in the 12 months to October, a big jump from September’s rate of 10.1%.

Retail sales rise in October

Official data shows that retail sales staged a partial recovery in October although more recent survey evidence suggests retailers remain relatively pessimistic about future trading prospects.

The latest ONS retail sales statistics revealed that total sales volumes rose by 0.6% in October, following a 1.5% decline during the previous month when shops closed for the Queen’s funeral. Despite this partial rebound, ONS said the broader picture was that sales are still on a downward trend that has been evident since summer 2021 and that volumes remain below pre-pandemic levels.

Survey evidence also highlights the current difficulties facing the retail sector, with the latest Distributive Trades Survey from the CBI showing the net balance of retailers reporting year-on-year sales growth falling from +18% in October to -19% in November. A similar proportion also said they expect sales to fall this month suggesting most firms anticipate little festive cheer this December.

Commenting on the findings, CBI Principal Economist Martin Sartorius said, “It’s not surprising that retailers are feeling the chill as the UK continues to be buffeted by economic headwinds. Sales volumes fell at a firm pace in the year to November, and retailers remain notably downbeat about their future business prospects.”

It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding and can be subject to change without notice and the accuracy and completeness of the information cannot be guaranteed. It does not provide individual tailored investment advice and is for guidance only. Some rules may vary in different parts of the UK. We cannot assume legal liability for any errors or omissions it might contain. Levels and bases of, and reliefs from, taxation are those currently applying or proposed and are subject to change; their value depends on the individual circumstances of the investor. No part of this document may be reproduced in any manner without prior permission.